Trends

For data-driven stories, to appear under “Trends” menu

With sky-high prices and ruthless mortgage rates, Halloween decorations aren’t the only thing making the housing market a little bit spooky this fall.

The median price of a new home sold during the month fell to $418,800 from $433,100 in August, the U.S. Census Bureau and the U.S. Department of Housing and Urban Development reported.

Seattle still has a ways to go in recovering from the Covid-19 pandemic, according to a report from the University of Toronto.

If you aren’t looking closely enough, you might miss it. The most expensive new listing in Seattle is a minimalist property that blends right into the Puget Sound scenery.

From entertainment and dining to community camaraderie, Capitol Hill is one of the trendiest neighborhoods in the country … so how much does it cost to live there?

The median existing-home price for all housing types in September was $394,300, up 2.8% from $383,500 in September 2022.

Specifically, single-family homes were built at a seasonally adjusted annual rate of 963,000, up 3.2% from 933,000 in August and up 8.6% from 887,000 a year earlier, according to government figures.

Brutalist style and sensory gardens may seem at odds — but they are both hot home design trends that will rule 2024. At least, according to new predictions from Zillow.

That ranking probably won’t come as a surprise to most Seattleites, though — residents of the Puget Sound area are likely well aware of the city’s strengths in sustainability.

A 15% rise in applications for adjustable-rate mortgages drove overall mortgage applications higher in the most recent weekly survey.

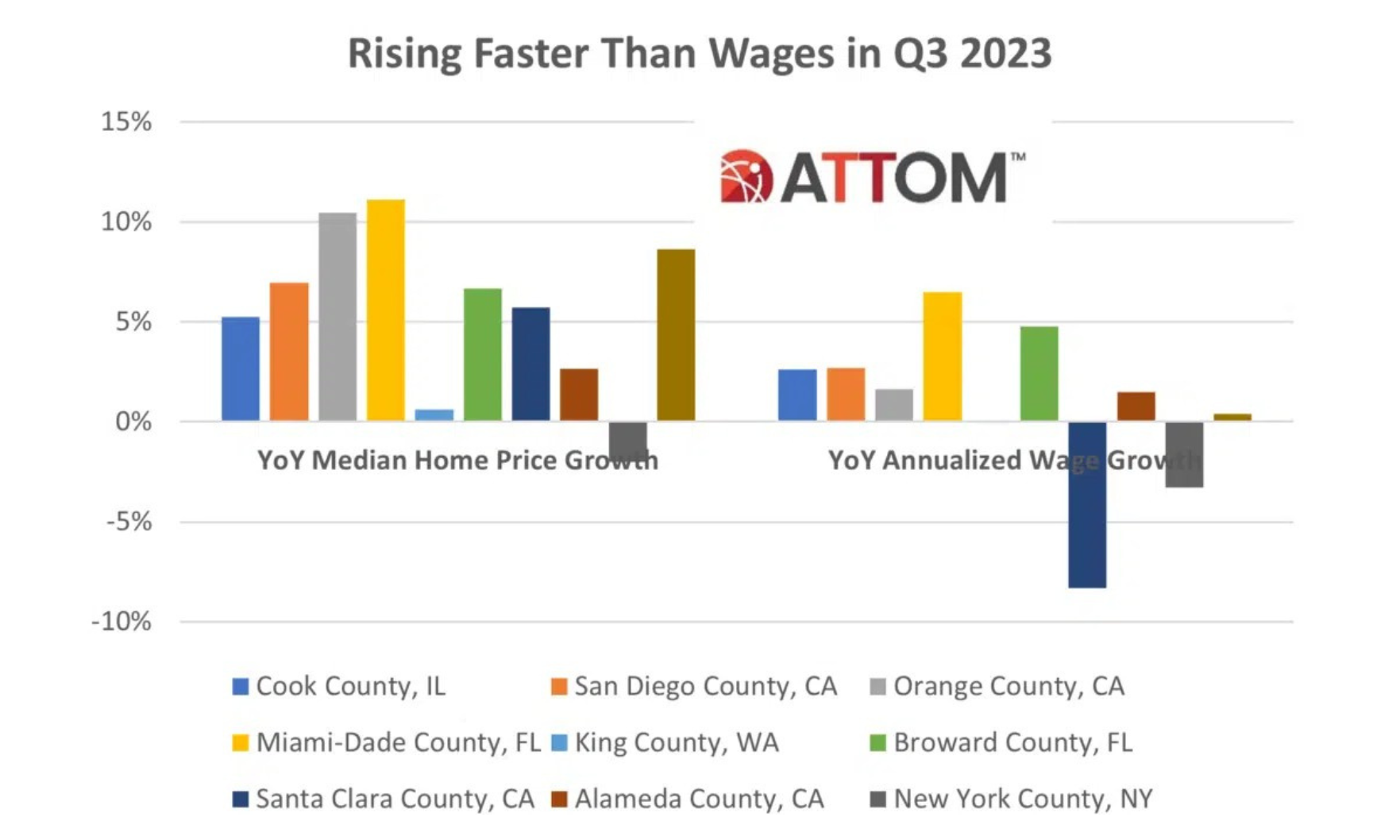

In King County, prices rose by 1% annually in Q3 — and that appreciation outpaced local wage increases, as in 47% of counties analyzed.

Point2Homes analyzed listings in every U.S. state and Washington, D.C. to determine the most expensive home for sale in each.

Regionally, pending sales were down across the board on both a monthly and an annual basis, the National Association of REALTORS® said.

Among the top upgrades: large showers.

Total housing inventory at the end of August was 1.11 million units, up 3.7% from July but down 14.6% on a year-over-year basis, the National Association of REALTORS® said.

All listings were posted within the last 30 days in the city of Seattle.