Current Market Data

More than 4,500 homes in the Seattle metro area have sold for more than $100,000 over their asking prices this year, and 580 of those fetched more than $300,000 over the asking price, according to a new Redfin report.

Market competition has eased up recently, but seven in 10 buyers still face bidding wars, according to a new report from Redfin.

Inventory levels rebounded last month, finally showing signs of recovery following a year of historical declines.

The typical increase in home sales as summer approaches failed to materialize nationwide last month, with average sales dropping 0.2% from April to May, while month-over-month sales in Seattle bucked the trend slightly, climbing 0.4%, according to the RE/MAX May National Housing Report.

Although pending sales are up 29% from last year, they are starting to slow down, dropping 9.7% from their peak four weeks ago.

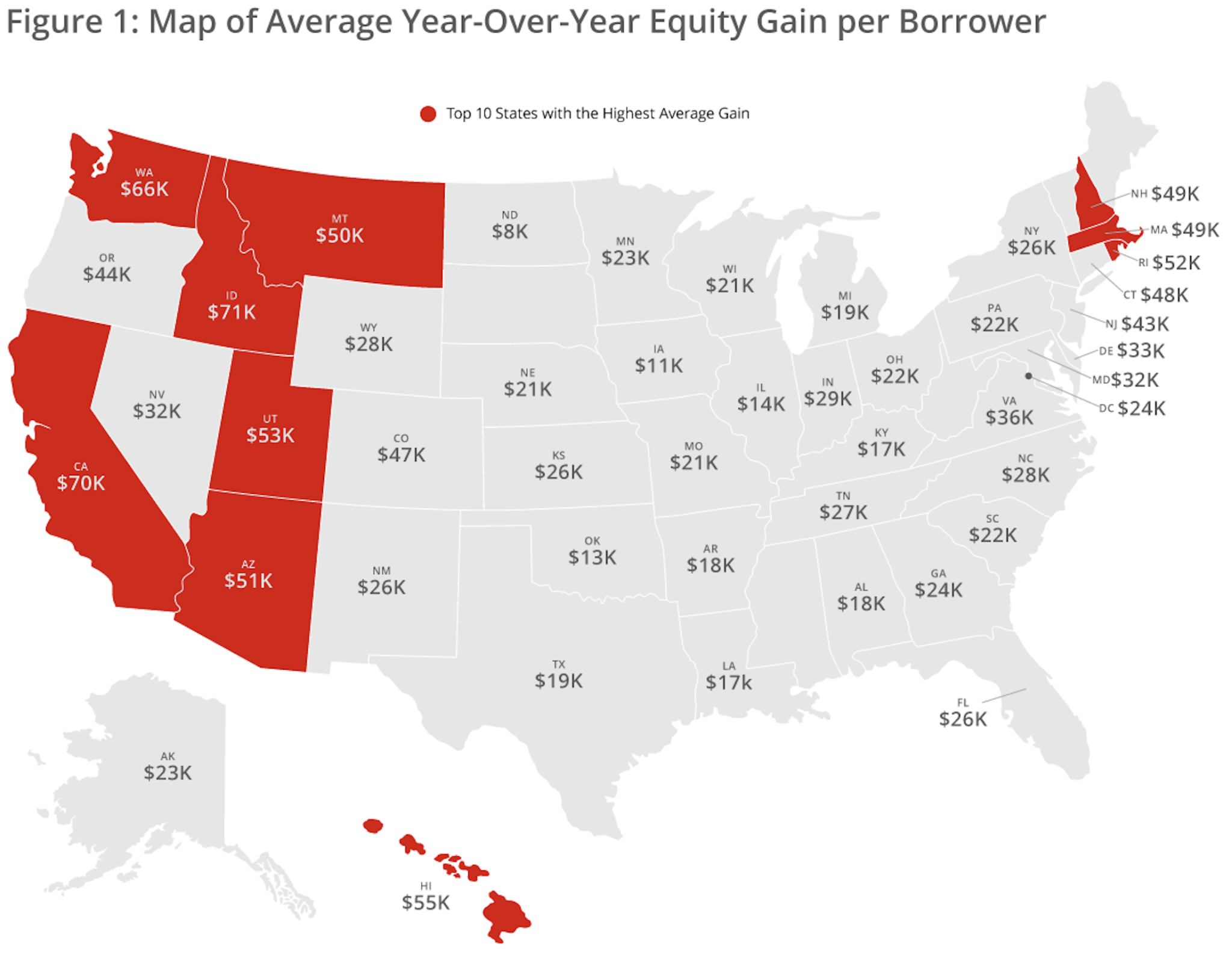

The rise in equity could help stave off foreclosures because homeowners can tap into that equity and sell their home, unlike during the 2008 financial crisis when many homeowners found themselves underwater in their mortgage, according to CoreLogic.

Experts at Builder Magazine recently came out with their Local Leaders list for 2020, which ranks the country’s 50 largest new-home markets based on closings by the end of the year.

Rising property values had homeowners cashing out of their existing residences to buy bigger homes in less-expensive areas last year.

Active listings for single-family homes dropped for the first time from April to May.

Pierce County led the way with a 61% increase in single-family permits.

High-end home sales surged in the three months ended April 30 as prices also rose and listings increased.

Sellers keep winning, while the pandemic and a strong economy are redefining long-held notions about metro Seattle’s real estate market.

Home-price growth remained in double digits for the 10th straight month in May as inventory lows pushed the median listing prices up 15.2% from last year.

Year over year, however, pending home sales were up 57.1%, the NAR said, citing its monthly Pending Home Sales Index.

First-time homebuyers found their long-term plans changed due to COVID.

The median sales price of new homes sold in April was $372,400, up from $334,200 in March and $310,100 a year ago.